Now Reading: Roadmap for a space-to-space economy

-

01

Roadmap for a space-to-space economy

Launch is the foundation of the space industry, to the point that many conflate it with the space industry in entirety because it is literally the loudest, most spectacular element we see. But the quietly orbiting satellites overhead are what really drive the space economy. Even if launch capabilities drastically increase as SpaceX promises with Starship, satellite deployment bottlenecks will continue to hold the space economy back. The satellite industry is now doubling the number of active objects in low Earth orbit (LEO) every two years, a growth rate with which no plausible expansion of launch capacity can keep pace.

A direct consequence is mounting orbital congestion. Satellites must continuously maneuver to avoid collisions, consuming propellant that drives up cost and limits mission life. Thus far, industry response is to deorbit at the end of life, destroying and scattering space-grade hardware and critical minerals that have already paid the launch cost. As congestion worsens, the cost of doing nothing compounds: more propellant per satellite, shorter missions, higher replacement rates and a continued launch bottleneck.

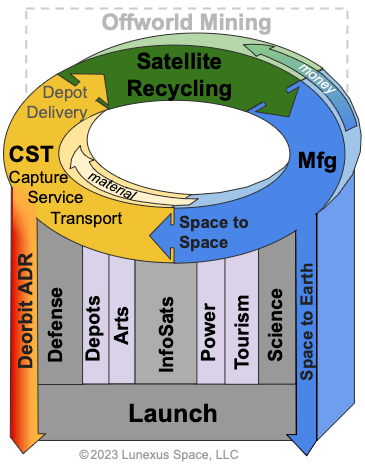

If the space industry is to flourish beyond this ceiling, it must embrace a space-to-space (S2S) economy that instead consolidates resources on orbit and produces space infrastructure local to where the demand is, generating commerce from space suppliers to space business customers and augmenting launch capabilities for satellite deployment. The S2S economy is an emerging and distinct part of the broader space economy, diagrammed here. Three sectors define its regenerative flow of materials and innovation: Capture/Service/Transport (CST) for orbital logistics, refueling and repair; Satellite Recycling for debris consolidation and materials processing into feedstocks; and In-Space Manufacturing for building hardware from orbital materials.

Such an economy requires a place to locally consolidate those critical resources: orbital depots. But infrastructure also requires processing technology and the societal systems that include funding mechanisms, regulation, procurement signals and institutional commitments.

The roadmap to get us to this economy needs to take us at least as far as a tipping point where commercial momentum can sustain the trajectory.

The roadmap

How do we recognize a tipping point, much less aim for one? Critical mass for a new market happens when key factors converge. The Internet provides a well-documented baseline.

| Tipping point factor | Internet analogy | Description in new markets |

|---|---|---|

| 1. Cost of access (the enabler) | Affordable PCs and dial-up modems | Barrier-to-entry cost must fall dramatically, making the core product accessible to developers and first users. |

| 2. Killer application (the lure) | Email and the World Wide Web browser | A high-value use case definitively better than the existing solution, compelling the first wave of customers. |

| 3. Infrastructure standardization (the foundation) | TCP/IP and HTML/HTTP standards | Core technical/legal protocols standardized and openly available, de-risking investment and enabling interoperability. |

| 4. Solve the chicken-and-egg (the catalyst) | First content creators and ISPs commit and flourish | Critical mass of both suppliers and demand must exist simultaneously, creating a self-reinforcing loop. |

| 5. Government/institutional mandate (the validation) | Government divestiture of ARPANET; pro-commercial regulatory signals | Commitment from large institutions to rely on the new market, providing the first major stable revenue source. |

These five factors are not the only possible gates; others may substitute. But they act as road signs even when detours are required. Timing also matters: EV adoption failed in the early 1900s and succeeded a century later, with the same technology but radically different market conditions. Where does the S2S sector stand?

🌕 Enabler: Met. The barrier-to-entry cost for the satellite industry is governed by the mass launch price. Following an initial market-capture discount, SpaceX stabilized pricing at around $3.5 million per ton for most satellites deployed via Falcon 9. Demand is increasing exponentially while supply is constrained by the hard physical limits of orbital injection windows and available launch sites. SpaceX has no incentive to undercut its own market. Blue Origin with New Glenn may provide some competition, but demand will likely fill every available launch window. The enabling threshold has been crossed; further cost relief is neither likely nor sufficient to solve the S2S bootstrapping problem.

🌓 Lure: Halfway there. Very few materials sold on Earth are worth their launch mass cost. The prospective space-to-Earth downmass markets are estimated to reach $10-15 billion. Meanwhile, the existing commercial infosat manufacturing market is now over $22 billion, with operators already in LEO. This gap is the opportunity. The credibility threshold for orbital manufacturing is closing technologically, with the market identified and the customers already in orbit.

🌘 Foundation: Early stage. Even though two out of every three satellites in LEO are now Starlinks, the industry is far from a standard. Starlink’s design is highly proprietary and siloed into SpaceX’s vertical integration model, being imitated across the industry. CONFERS, the Consortium for Execution of Rendezvous and Servicing Operations, represents the beginnings of serviceability standardization. Necessary, but not sufficient for S2S circularity.

🌒 Catalyst: Stalled at the hard part. The CST sector has harvested accessible logistics work, but the longer-lead manufacturing and materials processing tasks remain underfunded. Investors sour on 10-year return horizons. Historically this is where the government steps up in strategic development, but U.S. funding agencies are increasingly adopting a venture capital mindset, conflating investment cost with budget and infrastructure ROI with near-term returns. The irony is acute: Space Force doctrine explicitly calls for satellites that can maneuver without regret, repositioning freely without fuel penalty. Yet no institutional mechanism exists to build the orbital depot infrastructure that would actually supply that propellant. Our doctrine demands this capability; the procurement posture defunds its prerequisite.

🌑 Validation: Moving in the wrong direction. What catalyzed the commercial web was not a government product; it was the government’s deliberate decision to step back from the ARPANET backbone while simultaneously signaling, through procurement and regulation, that it would be a paying customer of the new market. NASA’s current approach to LEO does the opposite. The ISS deorbit decision crystallizes this tension by spending approximately $1.5 billion to destroy 420 metric tons of critical space-grade materials, intended to clear the way for commercial LEO destinations. However, NASA’s April 2026 request for feedback on a government-owned crewed station marks a potential pullback from commercial approach entirely, keeping $1.3 billion in recurring operating cost on NASA’s annual budget. Neither approach makes economic or strategic sense.

The validation gap is the policy gap

Four of the five tipping point factors are at least partially in motion. What is stalling the S2S economy is not technology readiness, not market demand and not entrepreneurial ambition. The gap is institutional, and it has a specific shape. The tipping point analysis shows that each sector waits for the others; the structural solution is a persistent orbital depot that serves all three simultaneously: anchor point for CST operations, processing facility for debris feedstocks and material supplier for in-space manufacturing. A depot seeds the economy. That is precisely the infrastructure our government must enable before commerce can build and run the destinations. Infrastructure is more than hardware and trusses; it is the societal systems that create and sustain them.

Three concrete recommendations

The concluding recommendations are not simply aspirational. Each is actionable with existing statutory authority.

1. Reframe for depot infrastructure. An uncrewed orbital depot consolidating debris, providing propellant and processing materials is not a niche capability waiting for the crewed station market to mature. It is the prerequisite. The crewed station market cannot scale economically without it, and the commercial satellite market is headed for a structural ceiling without it. Policy that treats the depot as an optional future enhancement has the dependency arrow backwards.`

2. Establish a Space Infrastructure Bond (SIB). The government funds the roads; commerce runs the service stations. NASA’s Commercial LEO Destination program inverts this by subsidizing the destination while leaving the road unbuilt. Perennial reliance on uncertain appropriation cycles has hampered the space industry since Apollo. The proposed SIB alternative is a federally backed revenue bond, modeled on precedents like the TVA and Ex-Im Bank that financed strategic infrastructure when direct appropriations were unavailable. It decouples depot construction from NASA’s unreliable annual budget cycle, services debt through NASA and Space Force anchor contracts and orbital feedstock revenue and gives the American public a voluntary opportunity to invest directly in space infrastructure. Unlike taxes, participation is a choice. It provides new space businesses a nondilutive financial tool and the market a durable institutional signal.

3. Establish a debris consolidation incentive. The FAA’s withdrawal of its upper-stage deorbit rule in March 2026 is an object lesson in regulatory fragility. The economically correct incentive should price orbital mass consolidated to a processing depot preferentially to wastefully deorbiting it, or irresponsibly cluttering orbits. Deorbit destroys value and distributes metal particulates in the upper atmosphere; consolidation retains value and builds a supply chain; leaving debris in place devalues the orbital neighborhood. A consolidation credit answers the question every CST venture is currently stuck on: who pays? It clears the orbital highways without destroying critical materials, and kickstarts the market validation the S2S economy requires. It provides the equivalent of traffic rules through incentive, rather than through an ongoing enforcement burden.

Time to act

The space-to-space economy is not a dream. The technology is clear, the market demand is documented, the industry is trying to organize. What is missing is the institutional commitment that provides the foundational infrastructure for a functioning market.

The ISS decommission window is narrow and will not reopen. The 420 tons of space-grade material currently in orbit, supported by 25 years of partnership infrastructure, represents the single most cost-effective seed asset for an orbital depot that anyone will ever have access to. The Space Force wants satellites that can maneuver without regret. That doctrine requires propellant in orbit. Destroying the platform most suited to supply it, to avoid a short-term budget conversation, forecloses the very capability the national security community is asking for. “Maneuver without regret” is not physically possible when we systematically destroy the mass required to enable it. Catchphrases cannot change the reality or tyranny of the rocket equation.

All roads to a space-to-space economy run through the depot concept. The easiest road uses a nucleus that is already in orbit. The question is whether the institutions responsible for stewarding it recognize the opportunity in paving the way. If we want an economy on the moon, we must start with infrastructure in LEO.

Greg Vialle is founder of Lunexus Space and a 2022 finalist in NASA’s Orbital Alchemy Challenge. He writes about orbital economics and the space-to-space economy at lunexus.space.

SpaceNews is committed to publishing our community’s diverse perspectives. Whether you’re an academic, executive, engineer or even just a concerned citizen of the cosmos, send your arguments and viewpoints to opinion (at) spacenews.com to be considered for publication online or in our next magazine. If you have something to submit, read some of our recent opinion articles and our submission guidelines to get a sense of what we’re looking for. The perspectives shared in these opinion articles are solely those of the authors and do not necessarily represent their employers or professional affiliations.

Related Posts

Stay Informed With the Latest & Most Important News

Previous Post

Next Post

Advertisement

-

01Two Black Holes Observed Circling Each Other for the First Time

01Two Black Holes Observed Circling Each Other for the First Time -

02From Polymerization-Enabled Folding and Assembly to Chemical Evolution: Key Processes for Emergence of Functional Polymers in the Origin of Life

02From Polymerization-Enabled Folding and Assembly to Chemical Evolution: Key Processes for Emergence of Functional Polymers in the Origin of Life -

03Astronomy 101: From the Sun and Moon to Wormholes and Warp Drive, Key Theories, Discoveries, and Facts about the Universe (The Adams 101 Series)

03Astronomy 101: From the Sun and Moon to Wormholes and Warp Drive, Key Theories, Discoveries, and Facts about the Universe (The Adams 101 Series) -

04True Anomaly hires former York Space executive as chief operating officer

04True Anomaly hires former York Space executive as chief operating officer -

05Φsat-2 begins science phase for AI Earth images

05Φsat-2 begins science phase for AI Earth images -

06Hurricane forecasters are losing 3 key satellites ahead of peak storm season − a meteorologist explains why it matters

06Hurricane forecasters are losing 3 key satellites ahead of peak storm season − a meteorologist explains why it matters -

07Binary star systems are complex astronomical objects − a new AI approach could pin down their properties quickly

07Binary star systems are complex astronomical objects − a new AI approach could pin down their properties quickly